Property Neutral

Sector Outlook

- Indonesian real estate draws less foreign investment

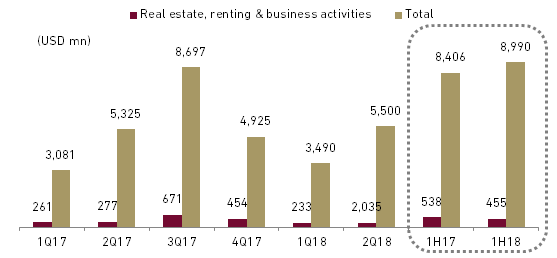

Indonesian property unequivocally sat on a downward trend with Foreign Direct Investment (FDI) in real estate sector slipped to USD455 bn in 1H18 or decreased by 15% YoY. The decline in real estate FDI contrary to total FDI growth which still improved 7% YoY to USD8.99 bn. Up to 1H18, the contribution of real estate FDI to total FDI stepping down by 134 bps to 5.06% from similar period in 2017.

Exhibit 92 : Indonesia FDI real estate and total

Source : BPKM, BI

However, we believe that Indonesia’s current massive infrastructure development is still attractive to overseas developer groups especially from Asian countries such as Japan and China. Local property developers such as BSDE, ASRI and BEST could be benefited from the inflow through the establishment of JVs with those foreign developers. We expect the situation could help mitigate the down cycle in local developer as we forecast Indonesian economic growth of 5.1% in 2019.

- Subtle growth in residential property

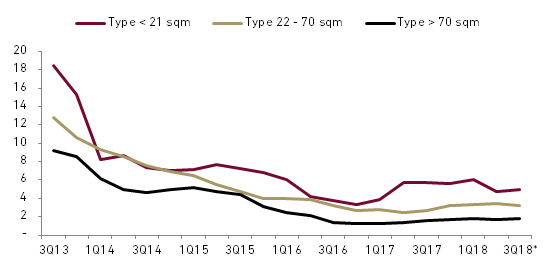

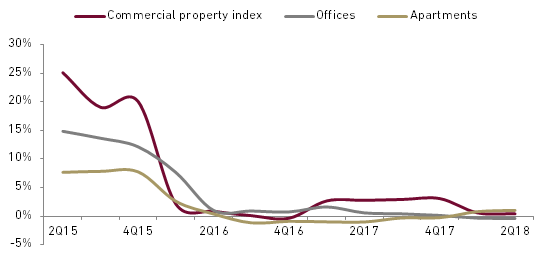

The residential property market is relatively in at better state compared to other subsectors as the growth in house prices were more sustainable at aggregate 3.3% YoY in 2Q18 and according to BI prediction will maintain at 3.3% in 3Q18. Other subsectors however, represented through commercial property index which is subdued at 0% YoY in 2Q18 with growth only shown by convention hall at 6% YoY thanks to seasonality. Meanwhile, industrial estates and apartments each grew by 1% YoY with other subsectors lagging at 0% to 2% YoY.

Exhibit 93 : Residential property price index based (% YoY)

Source : BPKM, BI

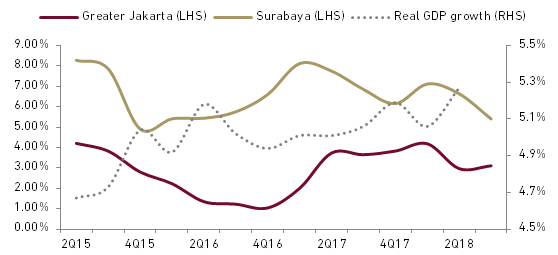

As we project real GDP growth to strengthen to 5.3% in 2019, we estimate the overall growth in house prices will remain flattish at 2%-4% YoY. We do not expect a strong price upsurge across the country unless the economy expands at a more rapid rate and overall confidence in the economy scales a new high. The house price index growth though still increasing annually, has been damped in the last three years and touched a new low of 2.4% YoY in 4Q16.

Exhibit 94 : Residential prices vs. real GDP growth (%, YoY)

Source : BI, BPS

- Interest rate hike pulls the brake on property sector

The prospect of property industry is currently pinned by three negative sentiments which are: 1) interest rate hike, 2) risk arises from political year, and 3) rupiah depreciation. Several property developers acquired negative free cash flow and low cash position hence has difficulty to pay their short term loans. Three companies with positive cash flow are PWON, BSDE, and DILD. Some of the companies hedge their US denominated loan up to Rp15,000/USD such as PWON and APLN, meanwhile BSDE and BKSL do not hedge their loan. Meanwhile, company with no exposure to USD loan is DILD.

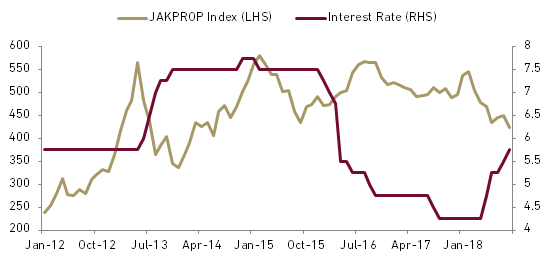

As of Sep 18, the 7 days RR stood at 5.75% which meant the benchmark has increased by 150 bps since the beginning of 2018. In Exhibit 4 we can see how JAKPROP Index has an inverse effect against interest rate.

Exhibit 95 : Residential prices vs. real GDP growth (%, YoY)

Source : Bloomberg, BI

In Jul 18, BI has lowered the Loan to Value (LTV) requirement up to 100% for new home buyers. However, market has shown lack of positive response to the aforementioned incentive and we expect the recent benchmark rate hike will send a fresh blow to already lethargic property industry.

Exhibit 96 : Indonesia commercial property index growth (%, YoY)

Source : BI

The extremely slow price appreciation of high-rise residential properties in Jakarta reflects the abundance of supply of such development. However, house price appreciation should be more pronounced in the coming years due to 1) traction gained from the MRT and LRT development within Greater Jakarta, 2) renewed confidence due to the economy’s strong performance, and 3) increasing scarcity of land closer to the urban centres.

- Commercial property prospects mixed

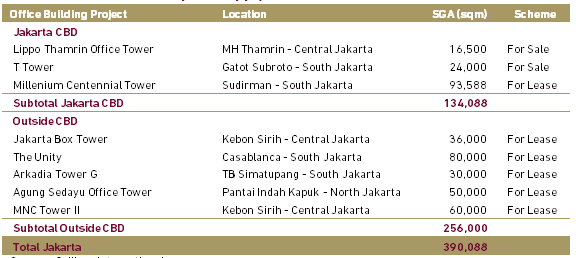

We expect slower rate of new commercial spaces in Jakarta as the last two years supply has been abundant. According to Colliers International, there will be a total of 390k sqm of newly available office space in 2019, almost 30% less than new office space scheduled to complete in 2018. The new office space will be coming in from three towers within Jakarta CBD and 5 towers on outside CBD.

Exhibit 97 : New office space supply in 2018

Source : Colliers International

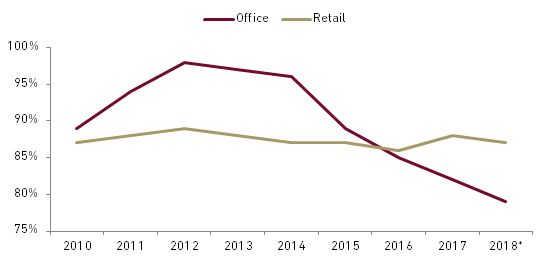

In line with the drop in occupancy rates, rental rates also came under pressure and were flattish. The office occupancy rate in Jakarta CBD is at all time low 79% expected by the end of 2018.

Exhibit 98 : Occupancy rates in Jakarta

Source: Colliers International, Ciptadana Estimate

We see limited positive catalyst for property industry hence NEUTRAL view. However, based on RNAV all of the stocks are undervalued hence attractive to investors with longer horizon. We pick SMRA, PWON and DILD as top pick based on their stable performance which likely to sustain in the coming year.

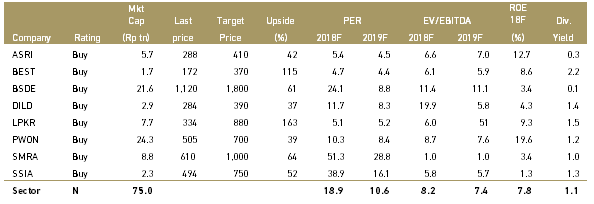

Exhibit 99 : Property stocks rating and valuation